Personal Finance Habits and Process

I believe that systems beat goals and habits beat checklists. In order to incorporate personal finance consistently into my process, I’ve used a few techniques. One of those is to turn the activities into habits. The other is to tack those onto already existing habits I already perform regularly.

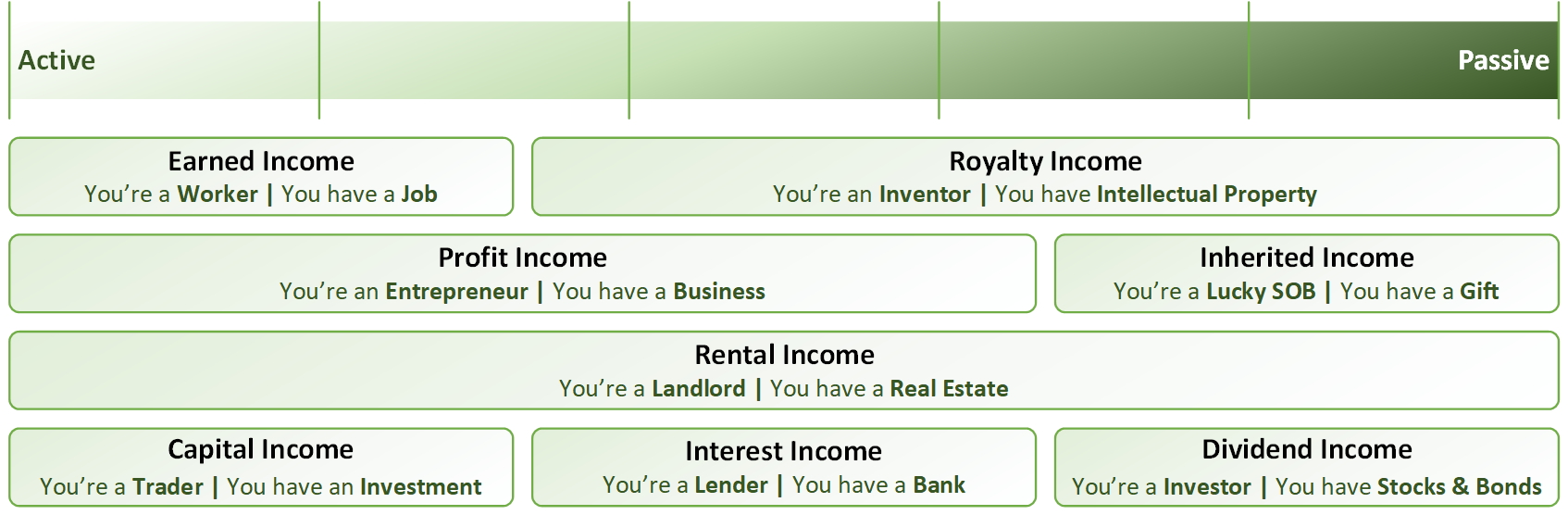

Eight Income Streams of Wealth Generation

The IRS breaks income into three types – earned, portfolio and passive. However, that is too simplistic for our purposes. If broken down not based on IRS qualifications,…

Basic Math: Trim Mean Average

A trimmed mean is a system of averaging numbers where a certain percentage of the smallest and largest values are excluded prior to calculating the average. In other…

Financial Planning Continuous Improvement

In my opinion, personal finance isn’t something that you do for a few weeks, months or years until you’re financially well off – and then stop. To be truly successful at building wealth, it needs to become a lifestyle. Something you just do. Like breathing.

Eleven Elementary Rules of Personal Finance

I like principles. I like rules. I don’t always follow them, mind you! And I certainly know when to purposely break them, in order to get where I need to be, or do what I need to do. However, I like getting knowledge that has been ‘tested’ out by people who came before me. Knowledge transferred saves me having to learn lessons the hard way.

Continue Reading Eleven Elementary Rules of Personal Finance

Basic Math: Geometric Mean Average

The geometric mean is the average of a set of numbers by using the product of their values, as opposed to using the sum, as in the arithmetic mean. The value of this method of calculating average can be seen commonly when calculating the performance of an investment or portfolio.

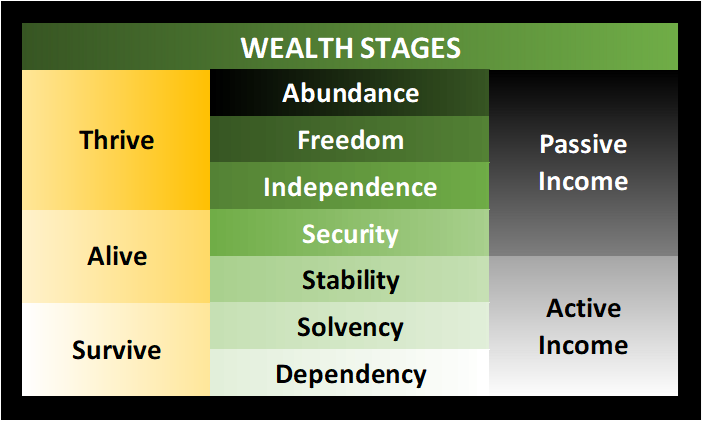

Seven Stages of Wealth Building

One of the biggest problems I had when I was first starting my Personal finance journey was figuring out what were reasonable targets. I wanted a more definitive set of targets to strive for that also had a basis in real changes to one’s quality of life, stage of living, wealth position, etc.

I wanted these targets to be

Net Worth Components

You can break out assets and liabilities into short term/liquid and long term/non-liquid. This allows you to differentiate between assets that could be accessed quickly and without penalty (market or regulation) and those longer-term assets where we would pay a price penalty to convert them to cash for immediate use. Additionally, breaking out we see what we owe in the immediate near-term vs longer term debts.

Recent Comments